- How Much Money Is Needed To Invest In Rental Property?

- Should A Real Estate Investor Get An Agent’s License?

- 5 Big Factors That Affect The Costs Of Renovating Your Home

- SIBOR Hike – What You Can Do With Your Current Loan

- 6 Basic Don’ts Of Real Estate Negotiation Tactics

- Will New Condo Relaunches Trigger The Great Property Sale We Have All Been Waiting For?

- 10 Proximity Amenities That Add Value To Real Estate

- How To Get Personal Loans More Easily With Good Credit

4 Financial Ratios To Judge Your Credit Position

It is hard to argue with someone who insist that they are in the pink of health financially. Because only individuals themselves will truly know what ins and outs of cash flow they have each month. But if you are able to present facts in a fair manner, it is difficult to deny what those facts imply. It’s just like that classmate who boast too much about his studies in high school. Only when the test score come out does he realize that he is not as good as he made himself out to be.

The good thing is there are ways to judge a person’s credit position quickly. With the use of financial ratios, an overview can quickly be drawn up to see on which part of the debt spectrum a person stands on. Of the hundreds of financial ratios that accountants and business analysts devour with a smile on their face, 4 of them are the most commonly used for individuals. Avoid confusing them with investment ratios. Putting them together tells the best story of how healthy a person’s debt position is.

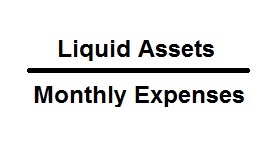

Liquidity ratio

This is an equation where the resulting number indicates the number of months expenses can be paid from current cash and cash equivalents if there is a loss of income. Meaning that if the result is 4, the household will be able to meet their expenses for 4 months without income. The higher the resulting number, the better position the person is in. A safe area figure to fall into would be between 3 to 6 months.

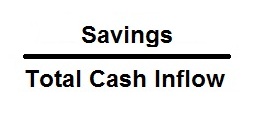

Savings ratio

This represents the amount cash inflow goes into savings as a percentage. While your mother might advice you to put everything you have into your minimum-interest savings account, that is not realistic in real life. Especially when you live in an expensive place like Manhattan when you have to think twice before having a proper fulfilling meal. Even though conventional wisdom suggest that you save as much as you can, as aggressively as you can, a 10% savings ratio is probably a fair amount for the average household.

Leverage ratio

This is an equation that reflects the level of your debt in relation to your assets. A high percentage reveals that you are highly leveraged as most of your assets are financed with debt or credit. With high leverage, you only need to lose your job to fully realize the mess that you are in. Creditors will start harassing you for payments. You will receive letters from debt collectors demanding payments disguised as law suits. And your spouse will start despising you for leaving the toilet seat up. You start fearing the call from the bank regarding foreclosure possibilities. And your friends secretly want to see your downfall so that they can start gossiping about it with their peers and colleagues.

A high leverage also suggest a low net worth. Lenders who put a lot of weight on net worth in credit analysis might avoid doing business with those of low or negative net worth. The prudent way to live financially is to only bite off what you can chew. But since times are changing and using other people’s money is championed around the investment world, a certain degree of leverage should be embraced. A ratio of not above 50% should keep anyone within the range of safety.

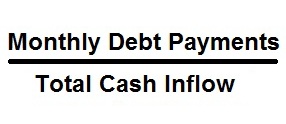

Debt service ratio

This ratio will reveal how much, as a percentage, income is used to service recurring debt obligations. Recurring debt refers to liabilities that are paid by instalments on a monthly basis. For example, vehicle loans, term loans, hire purchase, etc, are recurring debts. But do note that instalments do not necessarily refer to a fixed monthly payment amount. As in the case of mortgages, even though they are recurring payments that are taken into account for this ratio, adjustable interest rates can mean that monthly instalments are not fixed sums. A common reason is that a mortgage being pegged to the LIBOR index which floats according to market forces.

For different loan products, different levels of debt can be determined as a comfortable one. But on a personal financial point of view, a debt service level of not more than 35% can be deemed as financially healthy. A high level of debt to income will mean that you are prone to setbacks compounding when there is a loss of income or an increase in expenses.

Now that you are able to map out your credit position with an overview, it is important to remember that only you yourself is able to truly judge your predicament. That is because only you have intimate understanding of what is happening and what will be happening. Coming windfalls, bonuses, inheritance, other sources of income, etc, can sometimes make these ratios meaningless to you.

|

|

|

|

Latest Singapore home loan rates |

Hidden items that bring up mortgage costs |

Hiring a competent agent |

How to burn more calories in the office |

0 comments